AI Now Decides What You're Worth

What you do with AI is now the single biggest swing factor on what your company is worth, and treating it as optional is the most expensive decision you can make.

For years the playbook for a more valuable company was a familiar list: durable recurring revenue, customers that are not dangerously concentrated, a team that runs the place, and a founder who is not the single point of failure. That list is still right. But a new variable has moved to the top of it, and most owners have not noticed. The question is no longer just whether your cash flow is durable. It is whether your cash flow is about to be cheaper, faster, and harder to compete with, or whether it is about to be eaten by someone who moved first.

That question now decides what your company is worth more than almost anything else you control.

Value Was Never About the Past

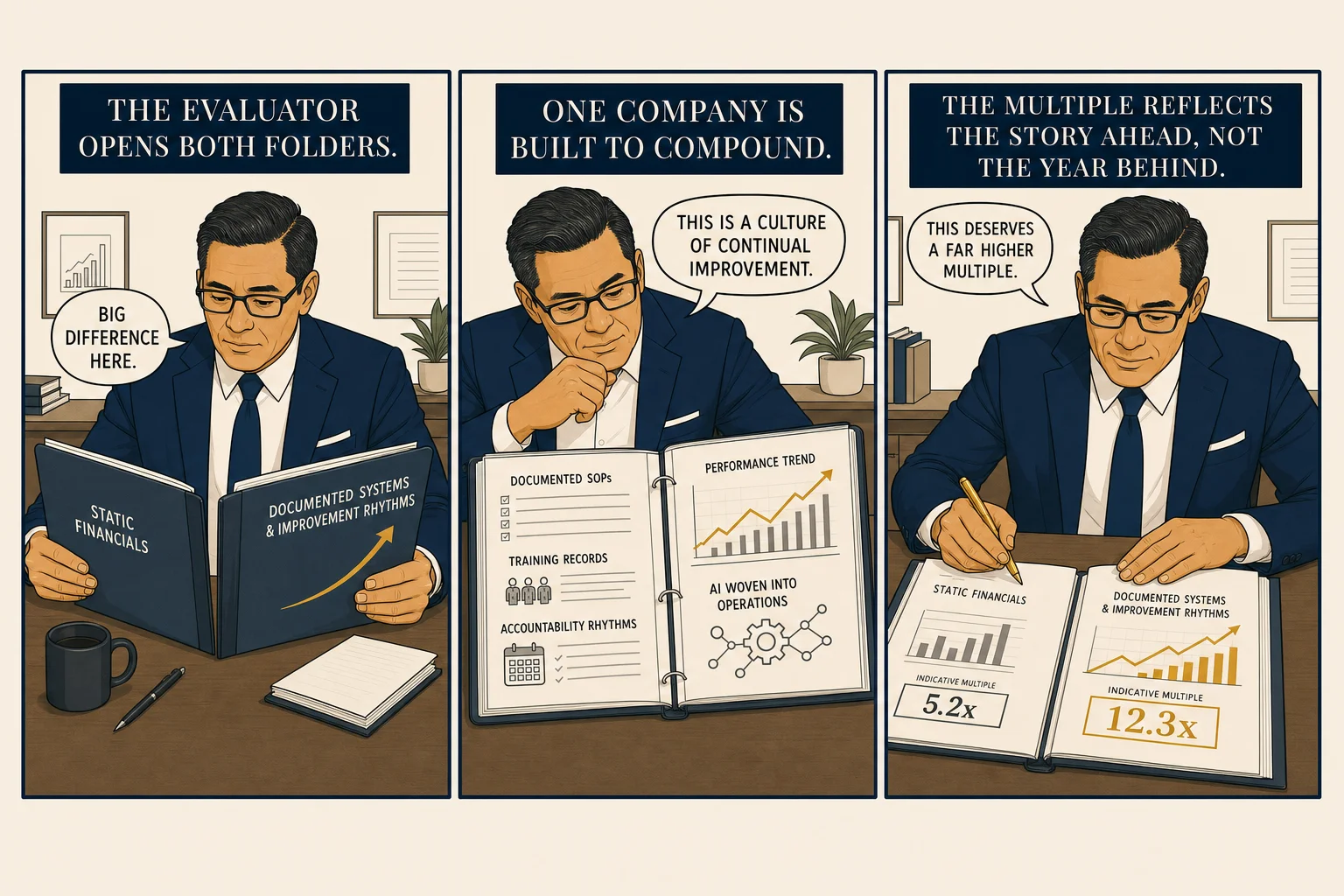

It is tempting to think a company's value is a reward for the profit it already booked. It is not. Value is a forward bet. When anyone prices a business at five or eight or twelve times its earnings, they are paying for the future those earnings predict, and how confident they are that the future keeps coming. The number is the present value of a story about tomorrow. Anything that changes the credibility of that story changes the number.

AI changes the story in both directions at once. A business that has wired AI into how it sells, serves, and operates tells a story of widening margins and a lead that compounds. A business that has not tells a story of a coming cost shock, where a competitor with better tooling underprices it and its durable-looking cash flow turns out to be a melting ice cube.

The Premium Is Real and It Is Measured

This is not theory. EisnerAmper's 2025 analysis of private-company valuations found that companies with demonstrably embedded AI are already valued materially higher than comparable peers, and those that look exposed are discounted. The spread is large enough to dwarf the swing you would get from a normal year of organic growth.

Put plainly: you can spend a year grinding out a few points of revenue, or you can move the same business into the category that is worth more per dollar of profit. One changes your value at the margin. The other changes which bracket you are in.

Why Doing Nothing Is the Expensive Choice

Owners tend to frame AI transformation as a cost and a risk. The honest framing is the reverse. The default path, doing nothing, is the one carrying the cost, because it is the one quietly compressing your value while you feel like you are being careful. The gap between how you run today and how a well-run version of your company would run on modern tooling does not disappear because you ignored it. It just becomes value you left on the table.

Stated once and set aside: this is also the whole commercial case for doing transformation well. Higher revenue, more operational efficiency, and, should you ever sell, a higher multiple. The point of this page is that the repricing is already happening, with or without you.

Not every company should transform right now

The repricing is a market reality you operate inside of, not a project deadline. Not every company needs AI right now, and for businesses whose processes are unproven or undocumented, a rushed implementation is more expensive than waiting — it signals execution failure to buyers and burns capital without improving the multiple.

The point is that doing nothing is not a neutral position. Your value is being repriced based on AI-readiness regardless of what you do. The choice is not "transform or don't." It is "get ready and transform, or stay unready and absorb the discount." Getting ready — documenting processes, proving functions, building the foundation — is itself the correct response to valuation pressure when you are not yet there.

What This Means for You

None of this argues for buying every tool and bolting a chatbot onto your website. Random AI spending impresses no one and reads as undisciplined. The premium goes to businesses where AI has changed the unit economics in ways you can prove with numbers, not slides.

That is why sequence matters. Before you can capture the premium you need a clear, ranked view of where AI actually moves your specific business, which is the argument in getting clarity before you transform. The one thing you cannot afford is to treat this as someone else's problem, because the value of your company is being repriced right now regardless of whether you participate.

Further reading

- Get Clarity Before You Transform

- The AI Valuation Premium

- Not Every Company Needs AI

- Why AI Now Sets Your Ceiling

- Service as Software

Sources: EisnerAmper 2025 on AI and business value; Built for Exit, "The Writing On the Wall"; Built for Exit, "Supersuit Up or Get Left Behind."